Future of Cross-Border Instant Payments

Cross-border payments – transactions where money moves from one country to another – are the backbone of global commerce and remittances. Yet historically, sending money abroad has been slow, expensive, and opaque compared to domestic payments.

Imagine waiting days for an international wire to clear and paying hefty fees, while local transfers happen in seconds. These longstanding pain points have spurred a worldwide push to modernize and enable instant cross-border payments.

In this article, we explore the future of cross-border instant payments, discussing emerging trends, regulatory perspectives (with a focus on the U.S.), and what a seamless global payment experience could look like.

The Cross-Border Instant Payments Future promises transactions that are as fast, affordable, and transparent as sending an email – a leap that could transform everyday finance and international business.

Understanding Cross-Border Instant Payments

Cross-border instant payments refer to international money transfers that settle virtually in real time (within seconds or minutes). This is a stark contrast to traditional cross-border payments that often take 1–5 business days to reach the recipient due to multiple intermediaries and time zone differences.

In the current system, a simple transfer from the USA to another country might pass through several correspondent banks, each adding delays and fees. According to the Bank for International Settlements, cross-border transactions today remain “slower, more expensive, less transparent and less accessible” than domestic payments.

These inefficiencies not only frustrate consumers but also hinder businesses that rely on timely international transactions.

The concept of instant cross-border payments envisions eliminating those lags. The goal is for a person or company in one country to send funds to another country and have them available to the recipient within seconds or at least under an hour, with upfront clarity on fees and exchange rates.

This would mirror the convenience of domestic instant payment systems (like real-time bank transfers or mobile payments) but on a global scale. Achieving this is challenging because cross-border payments involve different currencies, banking networks, and regulations on each side of the border.

However, advancements in technology and international cooperation are gradually closing the gap between domestic “fast payments” and cross-border transactions.

Why does the future point toward instant cross-border payments? In a digital economy, both individuals and businesses now expect immediacy. E-commerce sellers want quick settlement across borders; migrant workers want family remittances delivered in real time; travelers stranded abroad might need instant emergency funds.

The demand for speed, coupled with lower cost, is pushing providers and regulators to re-think how money moves internationally. In the next sections, we’ll delve into the current state of cross-border payments and the trends shaping their fast-paced future.

The Current State of Cross-Border Payments

To appreciate where we’re headed, it helps to examine where we stand. Traditional cross-border payments typically rely on the correspondent banking network – a decades-old system where banks hold accounts with one another to transfer funds.

While reliable, this chain-based process can be circuitous and slow. Each intermediary bank in the chain may take time to process the payment (often only during business hours) and deduct fees, resulting in cumulative delays and costs.

It’s not uncommon for international wire transfers to incur total fees of 5–7% (or more) of the amount sent when you combine bank fees and foreign exchange markups.

In fact, the global average cost of sending a $200 remittance was about 6.4% in late 2023, far above targets set by international bodies. This means a significant cut of cross-border payments currently goes to fees rather than to recipients.

Speed is another issue. Many cross-border transactions still take multiple days to complete. World Bank data and G20 analysis reveal that as of 2024 only roughly 69% of retail cross-border payments reach the recipient within one day, and just 33.5% arrive within one hour.

In other words, a large share of international payments are not yet fast by any stretch – nearly one-third take more than a day to be available to the beneficiary. This is well short of the G20’s goal that 75% of cross-border payments should be delivered within an hour by 2027.

High costs, slow speeds, limited access, and lack of transparency have been called out as the four key challenges facing cross-border payments. Senders often have little visibility into where their money is in the process or what exchange rate they got until after the fact.

These pain points have become more glaring as domestic payment systems improve. For example, within the U.S. you can send money instantly 24/7 using systems like Zelle or the new FedNow service – so why can’t a transfer to Europe or Asia be just as quick?

This gap has created opportunities for fintech innovators to step in with alternative solutions, and it has galvanized global regulators to prioritize reforms.

Despite the challenges, progress is underway. The volume and value of cross-border payments keep growing (about 5% year-over-year in recent data), showing robust demand.

The industry is huge: total cross-border payment flows were around $190 trillion in 2023 across all use cases, and are projected to reach a staggering $250–290 trillion by 2027–2030. (Most of that value comes from business-to-business transactions, which comprise the largest share.)

This growth is driving competition and investment in better infrastructure. Banks, payment processors, and tech firms are all racing to capture a slice of this expanding market by offering faster, cheaper services.

It’s worth noting that not all cross-border payments are equal – some corridors (country-to-country routes) have become much more efficient than others.

In fact, many cross-border payments between major currency corridors now settle same-day or even within an hour, especially for corporate transactions. However, in less developed corridors or certain remittance routes, payments might still be delayed and unpredictable.

This inconsistency is problematic for users who value certainty to run their businesses or support family abroad. Addressing the fragmentation in performance is a key part of future improvements.

The good news is that a combination of new technology and collaborative initiatives is poised to overhaul cross-border payments. Let’s explore the major drivers and trends shaping the future of cross-border instant payments.

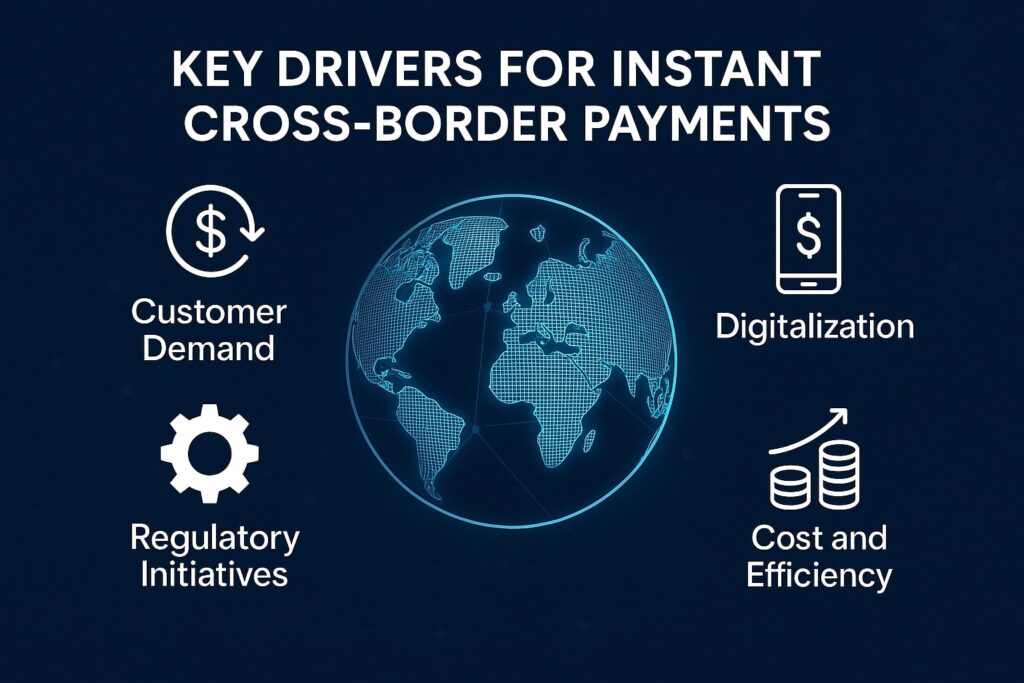

Key Drivers for Instant Cross-Border Payments

Several forces are converging to accelerate the adoption of instant cross-border payments:

- Customer Expectations: In an era of smartphones and on-demand services, both individuals and companies expect payments to move as quickly as information. The rise of e-commerce and gig work across borders means people don’t want to wait days for funds.

A real-time digital economy requires real-time payments. This pressure from end-users is perhaps the strongest driver – if one service offers faster transfers, customers will flock to it. - Technological Advances: Innovations like cloud computing, APIs, and distributed ledgers enable faster processing and connectivity between payment systems. Modern payment platforms can process thousands of transactions per second.

Technologies that didn’t exist decades ago – such as blockchain, artificial intelligence, and open banking APIs – now provide new tools to streamline cross-border flows. We’ll discuss these in detail in the next section. - Competitive Fintechs: Fintech startups and non-bank providers have entered the fray, often focusing on niche areas like remittances or small business payments. By streamlining routes and cutting out intermediaries, fintech providers can reduce transfer times and fees.

This competition is pushing traditional banks to modernize or risk losing business – a Citigroup study estimated banks could lose 5–10% of cross-border payment revenue to new entrants within a few years if they don’t adapt. - Global Economic Opportunity: As mentioned, cross-border flows are enormous (hundreds of trillions of dollars annually) and growing about ~5–9% each year. Tapping into this growth requires efficient infrastructure.

Countries see improved payment systems as a way to boost trade, investment, and financial inclusion. For example, exporters benefit from quick payments to manage cash flow, and migrants sending money home benefit from lower costs. The economic stakes are high, motivating both private and public sector action. - Regulatory Priorities: International bodies and national regulators have recognized cross-border payments as a priority issue. The G20 roadmap (2020–2027) explicitly aims to make cross-border payments faster, cheaper, more transparent, and inclusive.

Specific targets have been set (e.g., cut costs to under 3% and deliver most payments within an hour by 2027). The U.S. Treasury in a 2022 report also recommended prioritizing improvements in cross-border payments to enhance efficiency and even protect national security.

In short, there is high-level political will globally to support the transformation towards instant payments across borders.

In summary, the drive for cross-border instant payments comes from both bottom-up demand (users wanting better service) and top-down encouragement (regulators and industry strategists pushing for modernization).

With these drivers in place, the stage is set for significant change. Next, we’ll look at the technological innovations and solutions paving the way for instant cross-border payments.

Technological Innovations Shaping the Future of Cross-Border Payments

Technology is at the heart of the Cross-Border Instant Payments Future. A mix of innovations is redefining how money can move internationally, making the process faster and more efficient than ever before. Some key tech-driven developments include:

Real-Time Payment Networks and Interlinking

Many countries have implemented real-time payment systems domestically (for example, UK’s Faster Payments, India’s UPI, Brazil’s Pix, the EU’s SEPA Instant, and the U.S. FedNow/RTP). These allow bank transfers in seconds within each country.

The future lies in connecting these domestic real-time payment systems across borders. If the instant payment networks of two countries can talk to each other, a payment can hop from one to the other and credit a foreign recipient almost immediately.

There are already pilots proving this concept. In Southeast Asia, Singapore and Thailand linked their national fast payment systems (PayNow and PromptPay) in 2021, enabling instant low-cost transfers using just a mobile number. Transfers that once took days now complete in minutes, with fees dramatically lower than traditional methods.

By mid-2022, this Singapore-Thailand linkage was handling over 65,000 cross-border transactions per month, and senders who used to pay up to 10% in fees now pay around $4 or less per transfer (often under 1–2% for typical remittance amounts). This success story is serving as a blueprint for broader regional connectivity.

Likewise, banks and payment operators in the U.S. and Europe have launched a pilot called Immediate Cross-Border (IXB) to link U.S. dollar and euro real-time systems.

The Clearing House (operator of RTP in the US) and EBA Clearing (operator of RT1 in Europe) – with support from SWIFT – began testing instant payments between the U.S. and Europe, leveraging existing real-time rails.

Such pilots show that it’s technically feasible to bridge different countries’ systems and achieve near-instant currency transfers, at least for certain currency pairs (in this case USD↔EUR).

International organizations are working to generalize these links. The Bank for International Settlements (BIS) is spearheading Project Nexus, an initiative to connect multiple national fast payment systems into a network-of-networks.

If successful, Nexus would allow a payment sent in, say, India’s system to automatically route and deliver into Mexico’s or Nigeria’s system in real time, with currency conversion in between.

While full global interoperability is a tall order, these efforts underscore a key trend: interlinking infrastructure is a cornerstone of future cross-border instant payments. The more countries connect their 24/7 payment pipes, the closer we get to seamless worldwide transfers.

ISO 20022 and Data Standards

A less flashy but crucial innovation is the adoption of common messaging standards like ISO 20022 for payments. ISO 20022 is a rich data format for payment messages that enables more information to travel with a payment (like detailed remittance info, fees breakdown, sender/receiver data, etc.).

When all players use a common standard, payments flow more smoothly through the global system without data getting lost or needing manual intervention.

SWIFT, the global financial messaging network, has been migrating to ISO 20022 for cross-border payments, which improves compatibility between countries and banks.

Rich data standards also help with compliance checks (since required info like sender identity and purpose of payment can be included in structured form).

By 2025, many major payment systems worldwide will be ISO 20022-native, helping “speak the same language” and thus accelerating processing. In essence, harmonized data standards act as lubricant in the cross-border payments engine, reducing friction due to inconsistent formats.

Blockchain and Digital Currencies (Crypto, Stablecoins, and CBDCs)

Perhaps the most buzzed-about tech trend in cross-border payments is the use of blockchain and digital currencies. Blockchain (distributed ledger technology) allows value to be transferred globally without relying on the traditional bank correspondent network.

A number of developments in this space could influence the future of cross-border payments:

- Stablecoins: These are cryptocurrencies pegged to fiat currencies (like USD Coin pegged to the U.S. dollar). Stablecoins can be sent around the world on crypto networks 24/7, settling within minutes or even seconds on blockchains.

Unlike volatile crypto like Bitcoin, stablecoins aim to hold steady value, making them more practical for payments. Using stablecoins can bypass some banking intermediaries and reduce fees significantly, especially for small international payments.

For example, sending money via a USD-pegged stablecoin from the US to someone in another country can be near-instant and cost just pennies in network fees – though the recipient may then need to convert the stablecoin into local currency. Stablecoins operate continuously, so they aren’t limited by banking hours.

Large companies have started experimenting with accepting stablecoins for cross-border transactions (e.g., some satellite internet services accepting payments in stablecoin from customers in countries with unstable currencies), showing the real-world utility of this approach. - Cryptocurrency Networks: Apart from stablecoins, even major cryptocurrencies or their second-layer networks can facilitate fast cross-border transfers.

For instance, the Bitcoin Lightning Network allows instant value transfer by converting fiat money to bitcoin and then back to fiat on the other side, all in the span of seconds.

Fintech companies have built services where users don’t even realize cryptocurrency is used under the hood – they just see a fast, low-cost transfer. These crypto rails provide an alternative path when traditional routes are slow or costly. - Central Bank Digital Currencies (CBDCs): CBDCs are digital versions of national currencies issued by central banks. While primarily a domestic monetary innovation, CBDCs carry big potential for cross-border use if countries connect their CBDC systems.

Multiple central banks (including the U.S. Federal Reserve researching a digital dollar, the European Central Bank with a digital euro plan, and China’s digital yuan pilot) are exploring how CBDCs could improve cross-border payments.

One vision is that two CBDCs could be transferred peer-to-peer between central bank ledgers, allowing instantaneous settlement of international transactions with central bank backing.

Pilot projects like mBridge (involving central banks of China, Hong Kong, Thailand, UAE) have already tested cross-border FX transactions using prototype CBDCs, significantly shortening settlement time and reducing costs.

While still experimental, by combining the trust of central-bank money with the efficiency of new tech, CBDCs could overcome many pain points of today’s system (like reducing the dependency on long correspondent chains).

MasterCard predicts that as real-time payment systems and digital currencies become interoperable, it will be easier to transact between traditional bank accounts and digital currency wallets, further seamless cross-border transfers.

In summary, blockchain-based solutions offer the tantalizing prospect of near-instant settlement and round-the-clock availability for cross-border payments.

However, they also introduce new considerations around regulation, volatility (for non-stable crypto), and interoperability with the traditional financial system.

It’s likely that the future will see a hybrid model – traditional networks improved by new tech like AI (covered next) and selective use of digital currencies for specific use cases or corridors.

Artificial Intelligence and Automation

AI and machine learning are unsung heroes making instant cross-border payments more feasible. One major hurdle for instant payments across borders is handling all the necessary compliance and risk checks in real time.

Whenever money crosses borders, banks must screen for money laundering, terrorism financing, sanctions compliance, and fraud. Traditionally, these checks can introduce delays (for example, if a name needs manual review or a slight data mismatch causes an exception). AI is helping to automate and accelerate these processes:

- Fraud Detection & Security: AI can analyze patterns across millions of transactions to flag suspicious activities much faster than a human. Modern fraud systems use machine learning to catch anomalies and even predict potential fraud before a transaction is completed.

For instance, advanced AI models can instantaneously assess if a cross-border transaction is likely genuine or part of a scam, improving protection without manual intervention. - Sanctions and AML Screening: Rather than having compliance staff manually verify each cross-border transfer, AI-driven compliance engines can automatically check names against sanction lists, verify transaction purposes, and ensure all required data is present.

These systems are reducing false alarms and speeding up the green-lighting of legitimate payments. According to industry reports, AI-based automation can cut transaction processing times by up to 90% while also reducing operational costs by 30–50%, largely by minimizing manual work and errors.

This is crucial if we want instant cross-border payments – you can’t have a three-day delay for a compliance check on a payment that is supposed to settle in seconds. AI helps perform those checks on the fly. - Optimizing Forex and Routing: AI algorithms also assist in getting the best exchange rates or choosing the fastest route for a payment.

For example, AI can dynamically route a transfer through the most efficient corridor or intermediary based on current network conditions or liquidity, much like how internet traffic is routed for speed.

It can also predict and optimize currency conversion timing to minimize costs or volatility impact. These behind-the-scenes optimizations make the user experience smoother (funds arrive faster and possibly with a better rate).

In short, AI and automation act as the “smart engine” under the hood of instant payments, ensuring that the increasing speed does not compromise security or compliance.

Banks and payment providers are heavily investing in these technologies to enable scale: tens of thousands of cross-border payments per second cannot be manually monitored, so intelligent automation is key.

Interoperability and Open APIs

Another tech piece of the puzzle is improving interoperability through open banking APIs and partnerships. Many banks and payment companies are exposing APIs (Application Programming Interfaces) that allow different payment systems and fintech services to connect with each other seamlessly.

This API economy means a fintech app can initiate a cross-border payment through a bank’s backend system or vice versa, in real time, without manual file exchanges or delays.

For example, a multi-currency wallet app might use open APIs to pull funds from your U.S. bank account and send to a European bank account via an international payment network, all with a few clicks.

Standardized APIs and protocols (such as those promoted by initiatives like PSD2 in Europe) encourage a more connected ecosystem, which is critical for cross-border flows that inherently involve multiple providers.

Payment hubs and cloud-based platforms are emerging to orchestrate payments across networks. These act as central switchboards where an instant payment request from one country can be mapped and delivered into another country’s system through pre-built API connections.

In the near future, sending money abroad could be as simple for fintech apps as calling an API that abstracts all the complexity – the platform figures out the best route, handles compliance, and guarantees the funds transfer, nearly instantly.

The key takeaway is that technology – from payment network design to AI to blockchain – is solving many of the historical limitations of cross-border payments. However, technology alone isn’t the full story. In the next section, we’ll address how regulation and international cooperation factor into this future.

Regulatory Perspectives and Challenges (USA Focus)

Technology might enable instant cross-border payments, but regulatory frameworks need to evolve in parallel. Every cross-border transaction straddles at least two jurisdictions, meaning multiple sets of rules on money movement, data, and currency exchange apply.

A critical part of the future of cross-border payments is navigating these regulatory complexities in a way that still allows for speed and efficiency. Here’s a look at the regulatory perspective, especially from the lens of the United States:

1. Anti-Money Laundering (AML) and Compliance: Fast payments must still be safe payments. U.S. regulators (and their counterparts worldwide) are very focused on ensuring that speeding up payments doesn’t open the floodgates for illicit finance.

All the normal rules – verifying customer identity (KYC), monitoring transactions for suspicious activity, sanction screening – remain in force. The challenge is doing this in real time. The U.S. has strict AML laws (Bank Secrecy Act, etc.) which financial institutions must follow even for instant payments.

As mentioned, adopting global standards and technology like AI helps. The Financial Action Task Force (FATF), a global body, is updating guidance so that countries harmonize their AML measures for cross-border payments.

For example, the so-called “Travel Rule” now applies to cryptocurrency transfers as well, requiring certain sender/receiver info to accompany cross-border crypto transactions, akin to bank wires.

2. Data Localization and Privacy: Different countries have different rules on whether data about transactions can leave the country. Some jurisdictions require that payment data be stored locally.

For a U.S. payment going to, say, India (which has data localization rules), providers must ensure compliance with those laws, which can complicate truly instant processing. Privacy laws like Europe’s GDPR or various U.S. state laws might also impact how customer data in payments is handled across borders.

The industry is working on solutions like privacy-enhancing technologies and agreements that allow the necessary data to flow with payments in a compliant way.

3. Currency Control and Capital Rules: Some countries have regulations on how their currency is exchanged or limits on cross-border transfers. While the U.S. dollar is freely convertible, not all currencies are.

Instant payment systems will need to incorporate checks for any regulatory limits on certain corridors (for instance, if a country caps remittances or requires certain documentation for large outflows). Harmonizing these rules or at least making them machine-readable is part of the regulatory challenge.

4. U.S. Regulatory Stance on Innovation: The United States has signaled support for improving cross-border payments. An Executive Order in 2022 on digital assets and payment system innovation led to a Treasury report which explicitly said the U.S. should “prioritize efforts to improve cross-border payments” both to boost efficiency and protect national security interests.

U.S. authorities participate actively in the G20 cross-border payments roadmap and related international working groups. The Federal Reserve’s launch of FedNow (a domestic instant payment service) in 2023, while focused on U.S. transactions, lays the foundation for potentially linking with other countries’ systems in the future.

American regulators are also examining new tools like stablecoins: for example, Congress and the Federal Reserve have been assessing how stablecoins might be regulated, given their growing use in cross-border contexts.

Any federally issued digital dollar (CBDC) in the future could also have a huge impact on cross-border payments, and the U.S. is carefully studying that possibility.

5. Standardization and Collaboration: Regulators recognize that no single country can fix cross-border issues alone – it requires international cooperation. Hence, we see efforts like the G20 roadmap with 19 building blocks (covering everything from coordinating regulation to extending payment system hours).

The U.S. supports these and often leads in global forums for setting standards that reflect its values (for instance, insisting on privacy and human rights considerations in how global payment systems evolve).

One concrete standard effort is extending operating hours of key payment systems so they overlap more; another is adoption of ISO 20022 messaging which we discussed.

6. Sandboxes and Pilot Programs: To foster innovation while managing risk, regulators (including in the U.S.) have been open to fintech sandboxes and pilot programs. These allow new cross-border payment solutions to be tested with real transactions but under supervision.

For example, a blockchain-based remittance service might get limited approval to operate in a controlled manner to demonstrate its benefits and safety. Such initiatives help regulators learn and adjust rules as needed.

The U.S. OCC (Office of the Comptroller of the Currency) and CFPB have had innovation offices to engage with new payment startups. Internationally, many countries are doing similar sandbox programs, and sharing lessons through bodies like the Global Financial Innovation Network.

Key Regulatory Challenge – Striking a Balance: Ultimately, the regulatory perspective boils down to balancing speed and innovation with security and stability. Instant cross-border payments must still prevent fraud, protect consumers, and not undermine monetary controls.

Achieving this balance will require continued dialogue between the industry and regulators. The encouraging news is that regulators are not blind to the issues – they are, in fact, often driving the agenda to improve cross-border payments because it can enhance economic activity and financial inclusion.

In the U.S., regulators see improving global payments as not just an economic issue but also one of maintaining currency leadership and national security (ensuring that new systems are not dominated by adversarial powers or misused by criminals).

As we move toward the future, expect to see clearer regulatory frameworks for things like stablecoin usage, more bilateral agreements between countries to recognize each other’s payment regulations, and global standards that payment providers can build into their systems for compliance-by-design.

Market Trends and the Road Ahead

Beyond technology and regulation, market trends and business strategies are shaping the future of cross-border instant payments. Here are some notable trends and what they mean for the road ahead:

- Bank-Fintech Partnerships: Traditional banks are increasingly partnering with fintech companies to upgrade their cross-border payment offerings. Rather than being disrupted completely, many banks have chosen to collaborate – leveraging fintech innovation while providing scale and trust.

Surveys show roughly 62% of banks are working with fintech firms to improve cross-border payments. These partnerships yield new services like multi-currency digital wallets, integrated e-commerce payment solutions, and instant remittance apps backed by bank networks.

The result is a blending of strengths: banks bring compliance and broad reach, fintechs bring agile tech and user-friendly interfaces. This trend is expected to continue, meaning the lines between bank and non-bank solutions will blur in the cross-border space. - Embedded Payments in Platforms: A growing trend is embedding cross-border payment capabilities directly into other platforms.

For example, a freelance job marketplace might integrate an instant payout feature so that a client in one country can pay a contractor in another country instantly on the platform, without either party leaving the app.

Similarly, accounting or invoicing software used by small businesses could have a “pay invoice now (cross-border)” button that triggers an instant international payment.

This embedded finance approach is expanding the availability of cross-border payments to where users already are, improving convenience and adoption.

It’s likely that in the future, many people won’t even realize they are doing a cross-border payment – it will just be a seamless part of whatever service they’re using. - Focus on Retail and SMEs: Historically, large corporations had access to relatively efficient cross-border payment solutions (through corporate banking channels), but retail customers and small businesses suffered the worst delays and costs.

Market trends indicate a lot of innovation is targeting those underserved segments. Remittance providers, mobile wallet companies, and neo-banks are competing to win migrant consumer flows with instant, low-fee services.

Likewise, startups targeting small-and-medium enterprises (SMEs) now offer platforms that let an SME pay overseas vendors or receive international customer payments in near real time, with better currency rates.

This focus on retail and SME use cases means the future will hopefully democratize instant payments – not just something big multinationals enjoy, but also families and small entrepreneurs. - Transparency and Customer Experience: Providers are learning that to win market share, they must offer full transparency and great user experience. Simply being faster is not enough if a user doesn’t know what they’ll be charged or if the app is too complex.

Therefore, a trend is to provide upfront guaranteed quotes for cross-border transfers (including the exact exchange rate and fees) and tracking capabilities so both sender and receiver can see the status of a payment.

Much like tracking a parcel shipment, customers want to track money in transit. New services already offer this, and it’s becoming a standard expectation. The G20 roadmap also flags transparency as a key goal, ensuring senders know total costs and time estimates in advance.

Expect future payment platforms to come with real-time notifications (“Your transfer has reached the recipient”) and user-friendly interfaces that hide the complexity of multiple networks behind the scenes. - Lower Costs through Competition: With more players and technologies in the mix, the cost of cross-border payments is forecast to drop significantly over time.

The United Nations Sustainable Development Goals target an average cost of 3% for remittances, and the G20 aims for even lower (1% for many transactions).

While global average costs have frustratingly inched up in the last year (slightly higher in 2024 than 2023), the overall trajectory with instant payment tech is toward cheaper transfers.

Digital-native solutions have lower overhead than legacy correspondent banking, and as volume scales up, economies of scale can be passed on to consumers.

Moreover, competition – whether from fintech or from new multilateral payment networks – will pressure incumbents to reduce fees. We are already seeing zero-fee or minimal-fee international transfers in certain corridors where new entrants are active.

In the future, paying a large percent fee to send money abroad may become a thing of the past, much like per-minute charges for long-distance phone calls largely disappeared with internet telephony. - Global Cooperation and Interoperability: The market is also trending toward more cooperative models. For truly instant cross-border payments, banks, payment firms, and central banks in different countries must work together.

We see this in regional initiatives (like the ASEAN region linking networks) and in global projects (BIS Project Nexus, SWIFT gpi enhancements, etc.). There’s an understanding that interoperability is key – no single network will dominate all others, so the focus is on making them talk to each other.

Think of how the internet works: different networks interconnect via common protocols so that data (or money, in our case) can hop across networks smoothly. This cooperation is partly market-driven and partly facilitated by international bodies.

By 2025 and beyond, we should witness more cross-border payment corridors being opened through bilateral or multilateral agreements (for example, more country pairs like the Singapore-Thailand link). Over time, these could stitch together into a near-global web of instant payment connectivity.

Comparison of Traditional vs. Instant Cross-Border Payments

To sum up the progress and highlight the future state, here’s a comparison:

| Aspect | Traditional Cross-Border Payments | Future Instant Cross-Border Payments |

|---|---|---|

| Speed | 2–5 days (often with uncertainty) | Seconds or minutes (75%+ within 1 hour goal) |

| Cost | High fees (5–7% on average for remittances); hidden FX markups | Low fees (aiming ~1–3% or less); competitive FX rates upfront |

| Transparency | Limited tracking; sender often unsure of status until delivery | End-to-end tracking and status updates; full fee and FX disclosure before sending |

| Availability | Limited to banking hours; weekends/holidays delay processing | 24/7/365 operation (no cutoff times) – money moves anytime, even nights & weekends |

| Intermediaries | Multiple correspondent banks in chain; potential points of failure or delay at each | Fewer hops – direct network links or peer-to-peer exchanges; streamlined routes |

| Compliance Checks | Often manual or batch-processed, causing delays if flags occur | Automated in real-time using AI and shared data standards, reducing friction |

| Error Resolution | Slow investigation if something goes wrong (errors can take days to trace/rectify) | Faster feedback loops – immediate validation of details, and ability to reverse or fix within minutes due to richer data and network rules |

| Inclusiveness | Many individuals globally are unbanked or underserved, can’t easily send/receive cross-border | Greater inclusion via mobile wallets and fintech bridges that connect to instant payment networks; reaching people without traditional bank accounts |

Table: How the Cross-Border Instant Payments Future compares with traditional international payments. The future state promises dramatically improved speed and user experience, though achieving these outcomes universally will require continued innovation and coordination.

FAQs

Q1: Why are cross-border payments slower and more expensive than domestic payments?

A1: Cross-border payments involve moving money across different national banking systems and currencies. Traditionally, they rely on a chain of correspondent banks, which means a payment might pass through several banks (each in different countries) before reaching the recipient.

At each step, processing takes time (often only during local business hours) and fees are deducted. Additionally, currency conversion is needed if the sender and receiver use different currencies, which adds cost.

Compliance checks for international transfers are also more complex, contributing to delays and expense. In contrast, domestic payments typically stay within one banking network and currency, so they clear faster and cheaper.

Essentially, more intermediaries and checks = more friction. Efforts to simplify the process (fewer hops, common standards) and use technology to automate checks are aimed at closing this gap so that cross-border payments can approach the speed/cost of domestic ones.

Q2: What technologies will make truly instant cross-border payments possible?

A2: A combination of technologies is working together to enable instant cross-border payments:

- Real-time payment networks that operate 24/7 provide the basic rails for immediate transfer; linking these networks internationally is key.

- ISO 20022 messaging standards ensure that rich payment data travels with the money, reducing errors and allowing straight-through processing globally.

- Blockchain technology offers new pathways (e.g., stablecoins or CBDCs) to transfer value globally within seconds, without traditional bank delays.

- APIs and cloud platforms connect banks and fintechs, so a payment can be routed optimally through different systems.

- Artificial intelligence automates fraud detection and compliance checks in real time.

Each of these plays a part.

The future likely isn’t one single technology but an integration of many – for example, a payment might use AI to clear compliance, hop from one country’s instant payment network to another via a Nexus-like connector, and possibly use a digital currency for the FX conversion in between, all in seconds.

Q3: How are regulators ensuring that faster cross-border payments remain safe?

A3: Regulators are deeply involved in shaping the future of cross-border payments to maintain safety and security. They are updating rules and guidance so that compliance checks can be done at high speed (for instance, promoting adoption of systems that share required data instantly, and encouraging AI use for monitoring).

Bodies like the FATF have been pushing countries to implement consistent AML/CFT standards to avoid weak links. The G20’s roadmap includes several items focused on harmonizing regulatory requirements and removing unnecessary barriers.

In the U.S., regulators have emphasized that any new payment innovations (like stablecoins or CBDCs) must have built-in protections against illicit use. We also see regulatory sandboxes where companies can test new cross-border payment tech under oversight – this helps regulators understand risks and fine-tune rules.

Overall, the approach is “compliance by design” – integrating checks into payment systems from the start, so that increasing speed does not compromise controls.

Q4: Will blockchain or cryptocurrencies replace traditional networks like SWIFT for international payments?

A4: Blockchain-based systems (including cryptocurrencies and stablecoins) are complementary technologies that may improve or bypass parts of the traditional system, but they are unlikely to entirely replace networks like SWIFT in the near future.

SWIFT (which provides messaging for banks) and correspondent banking have vast global coverage and legal infrastructure – they’re deeply embedded in how money moves today.

What’s happening is that SWIFT itself is adopting new technologies (e.g., its gpi service provides near-real-time tracking and faster settlement), and exploring blockchain interoperability.

On the other hand, cryptocurrencies and stablecoins are providing alternative rails: for specific use cases (like remittances to countries with limited banking access or high inflation), using a stablecoin can indeed leapfrog slower bank channels.

Some fintech companies convert fiat money to crypto, send it over crypto networks, then convert back to fiat for the recipient – effectively using crypto as the “instant transport layer” while the user only sees their native currency.

Central bank digital currencies might also enable direct exchanges between central banks, cutting out middle steps. So, we might not see a single replacement, but rather multiple interoperable pathways.

Traditional networks could coexist with blockchain networks, and the choice might depend on the corridor, amount, and use case. The end goal is the same: get the money there fast with minimal cost.

Whichever method achieves that for a given scenario will be used – in some cases it might be a blockchain solution, in others an enhanced traditional network.

Q5: What is the U.S. doing specifically to improve cross-border payments?

A5: The United States has several initiatives and perspectives on this front:

- The Federal Reserve launched FedNow in 2023, which is a real-time gross settlement system for domestic payments.

While it’s U.S.-only, having a 24/7 instant infrastructure at home is a step toward being able to link with foreign systems in the future. The Fed is also extending operating hours of Fedwire (for large payments) to align better with other time zones. - U.S. agencies are actively participating in international efforts like the G20 Cross-Border Payments Roadmap and working through the Financial Stability Board (FSB) and Committee on Payments and Market Infrastructures (CPMI) on global improvements.

This includes sharing data, setting targets, and encouraging U.S. banks to adopt things like ISO 20022. - The U.S. Treasury’s report on “The Future of Money and Payments” (2022) explicitly recommends improving cross-border payments and notes it as important for economic leadership and national security.

It highlights support for developing global standards that align with U.S. values (like privacy) and leveraging new tech responsibly. - Regulatory clarity is being worked on for new players: for example, stablecoin legislation has been discussed in Congress to provide guardrails for stablecoin issuers, which would in turn make those digital dollars safer for cross-border use.

- Lastly, the U.S. is using its influence in bodies like the FATF to push for consistent AML rules so that payments can be faster without being riskier.

In practical terms, many U.S. banks are upgrading their cross-border platforms (often via partnerships, as noted) to offer customers faster services – partly spurred by competition and partly by the Fed’s focus.

So, while the U.S. hasn’t rolled out a specific “global instant payment system” unilaterally, it is adjusting its own systems and is heavily involved in the global cooperative approach to achieve instant payments.

Q6: When will we see truly global instant payments for everyone?

A6: It’s an evolving process – some progressive corridors and regions are already close to the ideal, while others lag behind. In regions like Europe, North America, and parts of Asia, the pieces are quickly falling into place: widespread real-time payment adoption, initial cross-border links, and regulatory support.

We may see a significant portion of cross-border payments (especially between major economies) become instant or near-instant by the mid-2020s to 2030. The G20’s target date is 2027 for substantial improvements (e.g., most payments under an hour, costs down to 1–3%).

On the other hand, truly global instant payments – including every developing country and exotic currency – might take longer. It requires infrastructure upgrades in less developed markets and broader inclusion (getting more people into digital finance).

However, innovations like mobile money and regional payment hubs are accelerating inclusion even in Africa and remote areas. So the gap is closing.

We likely won’t wake up to a single “Big Bang” moment where suddenly every cross-border payment is instant; instead, it will be a steady expansion of instant capabilities country by country, corridor by corridor.

If current trends continue, by 2030 a majority of routine cross-border transfers (think person-to-person remittances, e-commerce payments, SME trade payments) could be completed in real time or close to it.

The full realization of a seamless global network may be a bit further out, but it’s coming into focus on the horizon.

Conclusion

The future of cross-border instant payments is bright, promising a world where sending money internationally is as quick and straightforward as sending a text message.

Major strides in technology – from interoperable real-time networks to blockchain and AI – are addressing the pain points that once seemed intractable. Likewise, global collaboration through frameworks like the G20 roadmap is aligning efforts to reduce cost and delay.

In the United States and worldwide, stakeholders recognize that improved cross-border payments can unlock economic growth, enhance financial inclusion, and make everyday life easier for millions of people who work, study, or support loved ones across borders.

That said, realizing this future universally will take continued coordination between tech innovation and policy evolution.

The journey involves modernizing legacy systems, ensuring robust safeguards (so that “instant” doesn’t equate to “insecure”), and making sure that benefits extend to all countries and communities, not just the largest players.

As we have seen, some early examples – like the link between Singapore and Thailand’s instant payment systems – show what’s possible, cutting transfer times from days to minutes and slashing fees. Scaling these successes and connecting them together is the task of the coming years.

For the general public, the move toward cross-border instant payments means more control over your money. It means if you’re sending funds to family abroad, they can receive it right away when it’s needed.

If you’re buying something from an overseas seller, the payment can settle fast, speeding up delivery. Businesses large and small will benefit from better cash flow management and fewer headaches in international transactions.

In conclusion, the momentum is firmly toward a more instant, integrated, and intelligent global payment ecosystem. While challenges remain, the combined efforts of financial institutions, fintech disruptors, and regulators are steadily dismantling the old barriers.

The next decade is set to witness cross-border payments evolving from a cumbersome procedure to a smooth, largely invisible background function of the global digital economy.

The future of cross-border instant payments, in a word, is borderless – a world where money moves as freely and rapidly across countries as data does, fostering greater economic opportunity and connectivity for all.