Payment Rails: ACH vs. RTP vs. FedNow

The U.S. payment rails are networks that move money electronically between accounts. The main rails today are the Automated Clearing House (ACH), The Clearing House’s Real-Time Payments (RTP) network, and the Federal Reserve’s FedNow Service.

Each rail has distinct features and use-cases, which we explore below. These systems differ in speed, availability, cost, and reach, so understanding them helps businesses and consumers pick the right tool for each transaction.

Automated Clearing House (ACH): Traditional Batch Transfers

ACH is the long-established network for U.S. electronic transfers, created in 1972 by NACHA (then known as the National Automated Clearing House Association). It supports batch-processing of credit and debit transfers (push and pull transactions).

For example, when you set up direct deposit, your employer’s bank sends an Automated Clearing House credit to your bank. ACH also handles debit pulls (e.g. bill payments when you authorize a company to collect from your account).

Banks collect ACH requests and process them in groups during business hours. Traditionally, ACH settlements took 1–3 days, but same-day Automated Clearing House (introduced in 2016) now lets many transfers clear on the same day.

- Widely adopted: Every U.S. bank and credit union supports Automated Clearing House.

- Cost-effective: ACH fees are very low (around $0.11 on a $50 payment) compared to 1–3% card fees.

- Reliable: Account numbers don’t expire, making Automated Clearing House ideal for payroll and subscriptions.

- Protected: Consumers can dispute unauthorized debits for up to 60 days. Fraud rates on Automated Clearing House are very low (under 1% of volume).

Automated Clearing House limitations include slower speed (batch settlement) and limited operating hours. Transfers settle in grouped batches (often overnight) and only on banking days.

Reversing an ACH payment is possible (if unauthorized) but must follow strict NACHA rules. Overall, Automated Clearing House remains the “default” rail for most recurring or bulk payments due to its ubiquity and low cost.

Real-Time Payments (RTP): Instant Bank Transfers

RTP is a newer 24/7 instant-payment network launched by The Clearing House (owned by major U.S. banks) in November 2017. Real-Time Payments transactions are near-instantaneous: funds move from sender to receiver in seconds, any time of day.

Like ACH, Real-Time Payments transfers bank-to-bank, but unlike Automated Clearing House they settle immediately and irreversibly. Once sent, Real-Time Payments payments are final and cannot be revoked. Modern ISO 20022 messaging is used, allowing rich data (e.g. invoice numbers) to be included.

- Speed and availability: RTP processes payments in seconds 24/7/365.

- Immediate finality: Funds are available to the recipient immediately; no risk of reversal once sent.

- Enhanced data: Supports ISO 20022 messaging so remittance details can travel with the payment.

- Large reach: Over 950 institutions participate (as of 2025), covering about 71% of U.S. checking accounts. (When technical connectivity is included, >90% of accounts are reachable.)

- High limits: RTP transactions can be up to $1 million.

Drawbacks of Real-Time Payments include higher cost (banks set fees, typically above Automated Clearing House fees) and incomplete adoption. Smaller banks were slow to join Real-Time Payments initially, so some accounts still cannot send/receive via Real-Time Payments.

Also, RTP is push-only (credit transfers), so it can’t directly pull payments like Automated Clearing House. Nevertheless, Real-Time Payments is used for urgent transfers: for example, businesses pay invoices instantly, and P2P apps like Zelle use Real-Time Payments for instant transfers.

FedNow Service: The Federal Reserve’s Instant Rail

FedNow is the Federal Reserve’s real-time payments network, launched in July 2023. It is a publicly operated instant payment system that any U.S. bank or credit union (with a Fed master account) can join.

FedNow transfers clear and settle in seconds, 24/7/365, similar to RTP. The Fed built FedNow to ensure broad access to instant payments, particularly for smaller or regional banks that had not joined Real-Time Payments.

- Nationwide access: Any eligible bank or credit union can offer FedNow. By mid-2025, over 1,400 institutions (mostly community banks and credit unions) were connected.

- Speed and finality: Payments settle immediately and cannot be reversed by the sender, using the same ISO 20022 messaging standards as RTP.

- Risk controls: The Fed built in new controls. For example, as of 2025 banks can set custom limits on how much a customer can send or receive instantly.

- Competitive catalyst: FedNow complements Real-Time Payments, giving businesses and banks multiple real-time options.

FedNow’s limitations include its newness. Adoption is growing but still incomplete. Initially, the per-payment cap was $500,000, and only recently (June 2025) was it raised to $1 million. Smaller banks that are slow to upgrade their systems may take time to implement FedNow.

As of 2025, FedNow only handles domestic transfers (though future cross-border links are being explored). Nevertheless, FedNow significantly expands real-time reach: within two years it grew from ~600 adopters to 1,400.

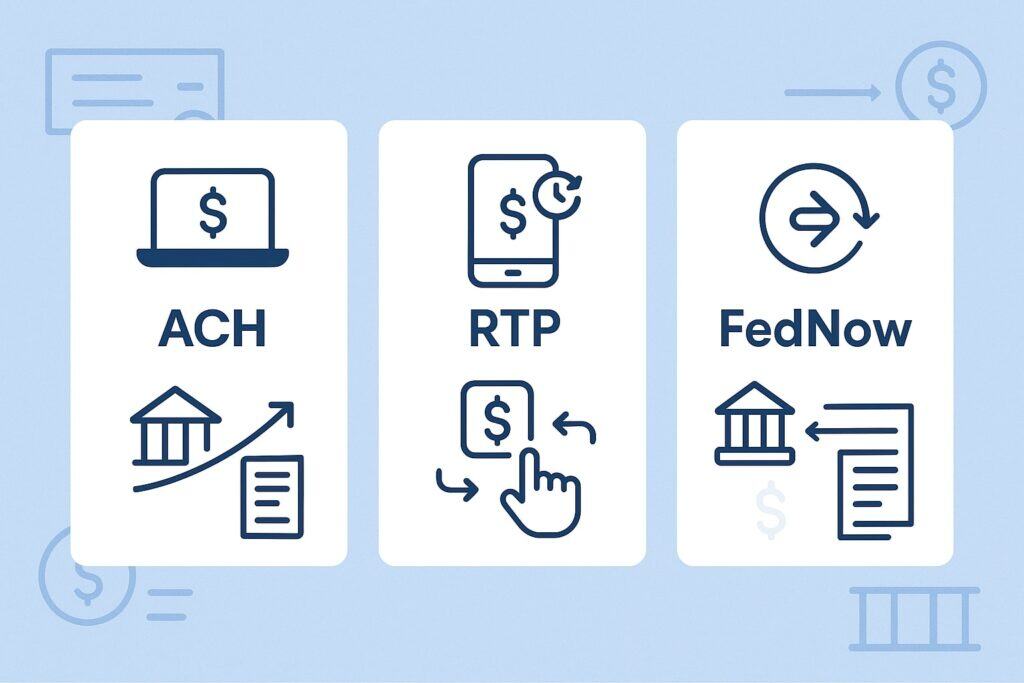

Comparing ACH, RTP, and FedNow

| Feature | ACH (Batch, NACHA) | RTP (The Clearing House) | FedNow (Federal Reserve) |

|---|---|---|---|

| Settlement Speed | 1–3 business days (now Same-Day option) | Seconds (24/7 real-time) | Seconds (24/7 real-time) |

| Availability | Batches during business days | 24/7/365 | 24/7/365 |

| Push vs Pull | Credit (push) & Debit (pull) | Credit-only (push) | Credit-only (push) |

| Funds Availability | Next-day (standard ACH); Same-day for urgent batches | Immediate (seconds) | Immediate (seconds) |

| Transaction Limits | Typically up to $100k per same-day NACHA rule (much higher for standard) | Up to $1 million | $1 million (since mid-2025) |

| Reach and Adoption | Universal (all banks) | ~950 banks (71% of accounts) | ~1,400 banks (95% community banks) |

| Fees / Cost | Very low (e.g. ~$0.11 per transaction) | Higher than ACH (set by providers) | ~$0.045 to send (sender pays) |

| Finality / Reversals | Reversible (60-day dispute window) | Irrevocable (final once sent) | Irrevocable (final once sent) |

| Typical Use Cases | Payroll, bills, subscriptions, B2B batch payments | Urgent B2B payments, P2P (e.g. Zelle), emergency pay | Similar to RTP (smaller bank focus), bill pay, payroll on demand |

- Speed: RTP and FedNow settle in seconds, much faster than ACH’s batch.

- Hours: ACH processes only in batches (during banking days), whereas Real-Time Payments/FedNow operate 24/7.

- Reversibility: ACH payments can be disputed by the originator (e.g. for fraud) up to 60 days. In contrast, Real-Time Payments and FedNow transfers are final and cannot be reversed by the sender.

- Data: Real-Time Payments and FedNow use structured ISO 20022 messaging for more data per transaction; ACH uses older formats.

- Cost: ACH is cheapest for high-volume batch transactions. Real-time rails often charge more (banks and FedNow have set higher fees). For reference, the Fed charges about $0.045 to send a FedNow payment.

Choosing the Right Rail

- Routine Recurring Payments: Use ACH for payroll, subscriptions, utility and loan payments. Its low cost and ubiquity make it ideal for large-volume, scheduled debits/credits.

- Urgent Transfers: Use Real-Time Payments or FedNow when speed matters. For instance, businesses settling an invoice on short notice or sending an emergency funds transfer benefit from instant settlement. Gig-economy payouts and real-time vendor payments also favor RTP/FedNow.

- High-Value Payments: With limits up to $1M, both RTP and FedNow can handle larger transfers instantly. For very large or cross-border transfers, wire systems (Fedwire or international networks) may still apply, but within the $1M range these rails are useful.

- Banking Relationships: If your bank offers it, consider enabling real-time rails in your payment platform. Many banks provide APIs or services (through processors like Modern Treasury, Dwolla, etc.) to send RTP/FedNow transfers directly.

In practice, businesses often use a hybrid strategy. They run high-volume recurring payments over ACH and reserve RTP/FedNow for just-in-time needs.

According to industry surveys, major companies are rapidly adopting instant rails: 40% of large (>$100M) firms already use Real-Time Payments, and nearly 70% expect to use instant rails (RTP or FedNow) within two years. This trend reflects customer demand: consumers increasingly expect fast, real-time payment options.

Use Cases and Examples

- Payroll and Gig Work: Companies can push same-day or instant payroll via FedNow/RTP to give employees immediate access to wages. A restaurant might pay delivery workers via Real-Time Payments that day, rather than waiting for standard ACH.

- Bill Pay and Invoicing: B2B suppliers can demand instant payment via an RTP or FedNow transfer. The emerging Request-for-Payment (RFP) feature lets vendors send digital invoices that customers approve for instant settlement.

- Peer-to-Peer (P2P): Consumer apps like Zelle and many banking apps use Real-Time Payments under the hood. Since 2021 Zelle payments have moved onto the RTP network, meaning P2P transfers arrive instantly. FedNow may similarly underlie new P2P tools offered by banks.

- Emergency Funds: In insurance or disaster response, instant rails speed critical payouts. A claim payout via FedNow reaches the customer instantly, improving cash flow and satisfaction.

- Treasury Management: Businesses use RTP/FedNow for real-time cash concentration and sweeping between accounts. For example, a company might use FedNow to instantly move excess funds from a regional account to HQ.

- Cross-Border Setup: While FedNow and Real-Time Payments currently handle U.S. domestic payments only, there is interest in linking them to global instant networks. (Global initiatives like BIS’ Project Nexus may eventually connect U.S. rails to systems like Europe’s SEPA Instant or Singapore’s PayNow).

Each rail fits different needs, so many fintech platforms and banks integrate multiple rails. For example, a payment gateway might send many payments via ACH for low cost, and fallback to RTP or FedNow when same-day delivery is requested.

Over time, as adoption grows, the choice will hinge less on bank connectivity and more on transaction requirements.

Industry Adoption and Trends

The shift to real-time payments in the U.S. has accelerated since FedNow’s debut. Key stats (as of 2024–2025):

- ACH volume remains enormous: the NACHA network processed over 33.5 billion ACH payments ($86.2 trillion) in 2024. Same-Day ACH alone handled 1.24 billion payments ($3.2T) in 2024, up 45% year-over-year.

- RTP growth: The Clearing House reports Real-Time Payments daily volume recently exceeded 1.18 million transactions (about $5 billion). In Q2 2025, 950+ banks sent 107 million RTP payments ($481 billion).

The year-over-year increase is significant: RTP payment volume grew ~32% in Q4 2024 to 98 million transactions. - FedNow ramp-up: FedNow’s adoption has been dramatic but from a small base. From 915,000 payments ($20 billion) in Q4 2024, FedNow’s annual volume hit 1.5 million transactions in 2024.

By early 2025, more than 1,200 institutions (mostly community banks/CUs) were alive. The Fed now updates figures weekly; trends show usage growing 2,000% year-over-year (though volumes are still tiny compared to ACH or Real-Time Payments). - Bank participation: As of mid-2025, Real-Time Payments has ~950 participating banks. FedNow has ~1,400 participants, of which ~95% are community banks or credit unions.

U.S. Faster Payments Council predicts that by 2028 about 75% of banks will be able to receive real-time payments (via either rail), though only ~35% may have full two-way capabilities by then. - Global context: U.S. was late to real-time payments compared to many countries. For example, Brazil’s PIX and India’s UPI process billions of instant transactions per year.

The U.S. now aims to catch up; the Fed and industry are exploring future links to global instant networks.

In short, all three rails are growing, but at different scales. ACH continues to dominate volume in sheer size. RTP and FedNow are increasing rapidly: industry observers note that FedNow’s launch spurred renewed focus on RTP growth, with daily Real-Time Payments volumes exploding after mid-2023.

The result is a more competitive landscape, which should spur faster innovation (e.g. enhanced remittance data, request-for-payment features, stronger fraud tools).

FAQs

Q.1: What is the difference between ACH, RTP, and FedNow?

Answer: ACH (since 1972) is a batch network (credits and debits) for routine transfers. RTP (launched 2017 by The Clearing House) and FedNow (launched 2023 by the Federal Reserve) are real-time credit-only networks. RTP and FedNow both settle payments in seconds, 24/7, while ACH settles in batches. Also, FedNow is Fed-owned, whereas Real-Time Payments is privately run.

Q.2: Who can use FedNow?

Answer: Any bank or credit union with a Federal Reserve master account can adopt FedNow. Once the bank joins, its customers (individuals, businesses, government) can send/receive instant payments through that bank. FedNow is designed to be accessible to institutions of any size.

Q.3: Which rail is fastest?

Answer: RTP and FedNow tie: both settle transactions in seconds, 24/7. ACH is slower: “same-day” ACH now completes within the same business day, but standard ACH takes 1–2 business days.

Q.4: How much does FedNow cost?

Answer: The Federal Reserve’s fee is about $0.045 per credit transfer sent (paid by sender). Receiving a “request-for-payment” costs $0.01. Actual bank fees on top of this may apply. For comparison, NACHA data show ACH transaction costs around $0.11 per transaction on average.

Q.5: Are RTP and FedNow available 24/7?

Answer: Yes. Both networks operate 24 hours a day, every day of the year. Payments can be sent and settled instantly even on weekends and holidays, unlike traditional ACH or wire hours.

Q.6: Can FedNow handle international payments?

Answer: Not yet. FedNow currently supports only domestic bank transfers. The Fed is exploring future cross-border linkages, but there is no direct international FedNow payment capability today.

Q.7: Is it true that FedNow will replace PayPal or Venmo?

Answer: No. FedNow is an additional rail for bank-to-bank transfers. It does not replace payment apps like PayPal, Venmo, Zelle or others. Those apps may use Real-Time Payments or ACH behind the scenes, but FedNow just adds another way for banks to send instant payments.

Q.8: Can I reverse an RTP or FedNow transaction if I change my mind?

Answer: No. Like cash, once a real-time payment is sent it is final. Neither RTP nor FedNow supports unilaterally canceling a payment after it is sent. ACH, by contrast, does allow a return/recall if an unauthorized debit is discovered. Users must be careful with instant payments.

Conclusion

ACH, RTP, and FedNow each serve different needs in the U.S. payments ecosystem. ACH remains the ubiquitous low-cost rail for high-volume and recurring transactions, while Real-Time Payments and FedNow provide speed and convenience for real-time transfers.

Together they give consumers and businesses more choice: for routine payroll or billing, ACH is often ideal; for same-day or on-demand transfers, instant rails (RTP/FedNow) are preferable.

The landscape is evolving rapidly – both Real-Time Payments and FedNow have seen strong growth, and ongoing enhancements (like richer data formats and request-for-payment features) are under way. In practice, many organizations will use a mix of rails (a “hybrid” approach) to balance cost, speed, and reliability.

Ultimately, ACH, Real-Time Payments, and FedNow complement one another. This healthy competition drives innovation and resilience in the payments system, benefiting fintechs, businesses, and consumers alike.

By staying informed about each rail’s capabilities and adoption status, financial professionals and small business owners can optimize how they move money – now and in the future.